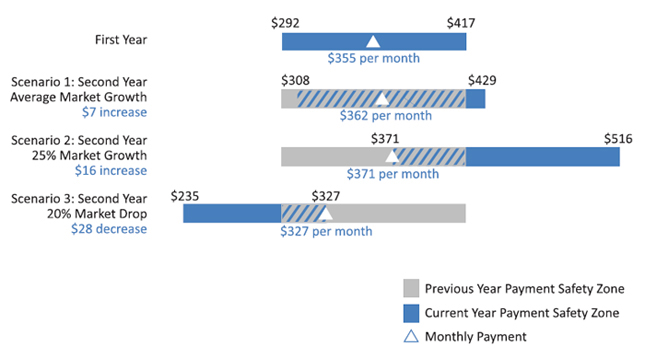

LifeStage Retirement Income—Calculating Monthly Payment Amounts

Example

Anne, who is in her mid-60s, has $100,000 in her Defined Contribution Account. She's preparing to retire and wants to begin monthly distributions. The illustration below shows the estimated monthly payment she would receive if she elects to manage her Defined Contribution Account through LifeStage Retirement Income. The illustration also shows her "payment safety zone"—the range of monthly payment amounts that have a high likelihood of helping her account balance last her lifetime.*

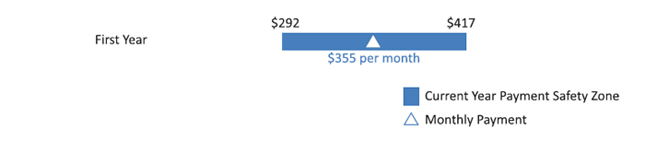

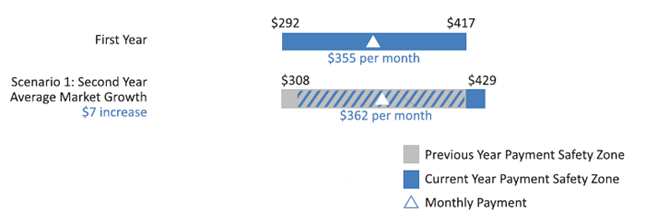

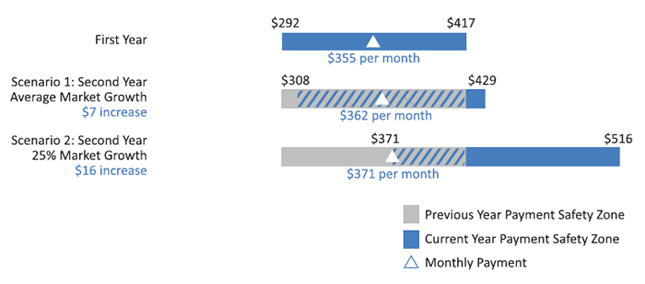

First Year

In the first year of retirement, Anne's monthly payments from her account would be approximately $355. The LifeStage Investment Management Service will continue to manage her investments. In a typical growth market, some of the withdrawn funds may be replaced or offset by investment gains.

Every November, LifeStage Retirement Income determines the cost-of-living increase for Anne's payment, recalculates her safety zone, and adjusts the payment amount if necessary to keep it within the safety zone. This "annual checkup" will occur as long as Anne remains enrolled in LifeStage Retirement Income.

Now let's look at three different scenarios for the second year.

Scenario 1–Second Year

In the first scenario, the cost-of-living increase is assumed at 2%, and the market gains and earnings on Anne's account match the amount she receives in monthly payments. Her payment increases by $7 to $362, falling within the new payment safety zone.

If there are large swings in investment returns, the payment safety zone may shift higher or lower. This change could cause Anne's monthly payment to be adjusted higher than the cost of living—or her payment could decrease.

Scenario 2–Second Year

In the second scenario, there is a significant 25% market gain.

Instead of a $7 increase, Anne's payment increases $16. The additional $9 added to her monthly payment keeps it within the safety zone.

Scenario 3–Second Year

On the other hand, if there is a significant market decline, Anne's payment could decrease.

In the third scenario, there is a sizeable loss in Anne's investments, yet LifeStage Retirement Income manages Anne's monthly payments so that there is only a minor impact on her monthly income, as shown in the illustration.