Investing Through Your Health Savings Account (HSA)

If you’re in a qualified high-deductible health plan (known in HealthFlex as an HSA plan), you can fund your HSA for 2020 with up to $3,550 a year ($7,100 family limit), and add up to $1,000 more if you are 55 or older. If you chose less than the limit initially, you can add to your account during the year.

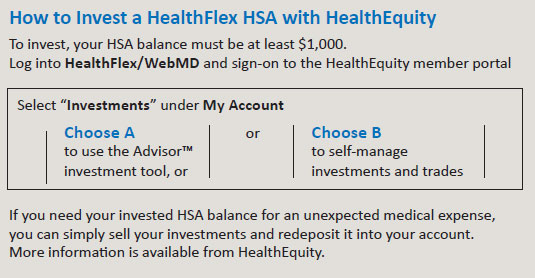

You probably already know that your HSA can help you save on medical expenses with tax-free contributions and withdrawals for medical expenses.* But did you know that the money you don’t use can be invested, earning interest and potential growth tax free?**

Unlike other tax-advantaged accounts, like flexible savings accounts (FSAs) or health reimbursement accounts (HRAs), the money you contribute to an HSA is yours—even if you change to a different plan or leave your job—and it can remain in the account indefinitely and even pass on to beneficiaries.

There are so many tax-advantaged account options [403(b)/401(k), HSA, FSA, etc.], that it can be difficult to decide how much to set aside for each one. To learn more read our “5 Reasons to Use an HSA” at wespath.org/r/hsareasons.

You can receive guidance from a financial planning professional at no additional cost by contacting EY Financial Planning Services at 1‑800‑360‑2539.***

* Qualified expenses are covered in IRS Publication 502 available at irs.gov/pub/irs-pdf/p502.pdf.

** This benefit is available in HealthFlex. Check your plan document to determine availability.

*** Costs are included in Wespath’s operating expenses that are paid for by the funds. Services are available to active participants and surviving spouses with account balances, and to retired and terminated participants with account balances of at least $10,000.