OCIO 101: How Do OCIOs Compare to Traditional Investment Consultants?

One of the biggest challenges for not-for-profit organizations is managing the investments that finance their missions. The Outsourced Chief Investment Officer (OCIO) model continues to gain attention as these organizations seek additional guidance with investment strategy implementation, asset allocation, investment manager selection and operations management.

Also read: OCIO 101: Why Organizations Are Outsourcing Their Investment Operations

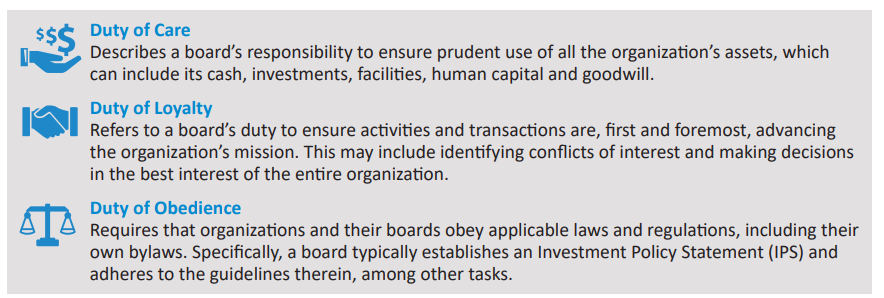

Fundamental Board Duties—Investment Management

The members of a board tasked with making investment decisions, typically an investment committee, must exercise three fundamental duties related to the stewardship of investment assets:

Given the importance of these core duties, it is not uncommon for boards and their investment committees to reflect on questions that may lead them to consider engaging the services of an OCIO. For example, is the board overwhelmed by the investment manager search and oversight process? Does the board have the investment expertise across multiple asset classes to confidently analyze, consider and implement recommendations? Can the board commit the necessary time to properly review and evaluate its policies on a regular basis?

While these are just a sampling of the considerations that might inspire a decision to outsource some or all of an organization’s investment activities, they help underscore the fact that unique organizations often grapple with similar challenges. These are exactly the challenges an OCIO can help them address.

OCIOs vs. Traditional Investment Consultants

Though interest in OCIOs is rising, it is not the only option available to organizations seeking help with their fiduciary responsibilities. Adding investment-focused staff is one idea, but the costs of developing a full-fledged investment team internally are quite high; an organization may need $1 billion or more in assets under management before it is able to justify considering that option. It is therefore common for not-for-profits to enlist some form of outside support to help manage their investments.

The traditional alternative to an OCIO is an investment advisory service or consultant. A chart comparing the service offering of an OCIO to a traditional consultant is highlighted below.

| Functions of the Service Provider | Traditional Consultant | OCIO |

|---|---|---|

| Designing investment funds and strategies? | Duties often shared with investment committee | Yes |

| Due diligence on prospective managers? | Yes | Yes |

| Manager selection and final approval? | No | Yes |

| Ongoing monitoring of managers? | Duties often shared with investment committee | Yes |

| Measuring and reporting on investment performance | Yes | Yes |

| Offer daily performance reporting and liquidity? | Sometimes | Sometimes |

As you can see, investment consultants provide several of the same functions as OCIOs, but they do not offer discretionary portfolio management services. OCIO services are closer to all inclusive, covering everything from fund design to manager selection and oftentimes daily performance reporting.

There are other factors to consider as well. For example, there can be special cost saving opportunities within the OCIO model; more simply, an OCIO’s scale may provide access to more unique, complex and exclusive investments at a lower cost than would be available to the organization otherwise. Boards may also uncover cost savings elsewhere when they can refocus their efforts and commit additional time to organizational efficiencies.

Operational factors also play a significant role when considering either the OCIO or traditional consultant model. A traditional investment consultant typically offers separately managed accounts (SMAs), or portfolios of individual securities managed by multiple asset managers. SMAs have their advantages, but they can be burdensome.

For instance, when investing in SMAs, an organization’s staff, not their consultant, is responsible for executing separate legal agreements with the asset managers, which consumes time and legal fees. This is even more challenging if the consultant recommends private or alternative investments, which have more complex legal documents.

In contrast, many OCIOs offer commingled funds, a type of pooled portfolio that combines the assets of several accounts, reducing the need for complicated administrative work.

The SMA structure may also require a more complicated accounting infrastructure. Organizations must monitor their custodian, ensure all entitled interest and dividends are received, reconcile account statements, and more. This process can be simplified with an OCIO. Clients of an OCIO do not need their own custodian; they benefit from the work of the OCIO’s custodian.

Boards, investment committees and their external service providers each play a vital role in the success of not-for-profit organizations’ investment programs. It is important that organizations find the right match for this collaborative effort.