Is Market Concentration a Risk? And Is Index Investing Making it Worse?

The infrastructure of the investment industry has changed a lot in the past 50 years. My grandparents used a phone to call their broker to buy and sell stocks in their portfolio. My parents’ generation experienced the growing popularity of mutual funds (and eventually, ETFs) and gradually expanded to buying and selling funds online or through a financial advisor. Today, my generation is a paradox: we speculate in online prediction markets, but we are also quietly funneling money into index funds through our retirement accounts on a regular cadence.

The advent of passive investments powered by technological advancement has broadened market access – lowering costs and making participation easier than ever before. Some have argued it’s also fueling today’s index concentration, as trillions flow into a relatively small number of benchmarks and, by extension, into whatever handful of companies sit at the top. Others would counter that concentration is cyclical – it existed long before the first index fund. Either way, the result is a market that looks broad on the surface but is increasingly narrow underneath. The question isn’t whether concentration exists — it clearly does. The question is whether it’s a risk, and, if so, what should investors do about it?

Who sits at the top today

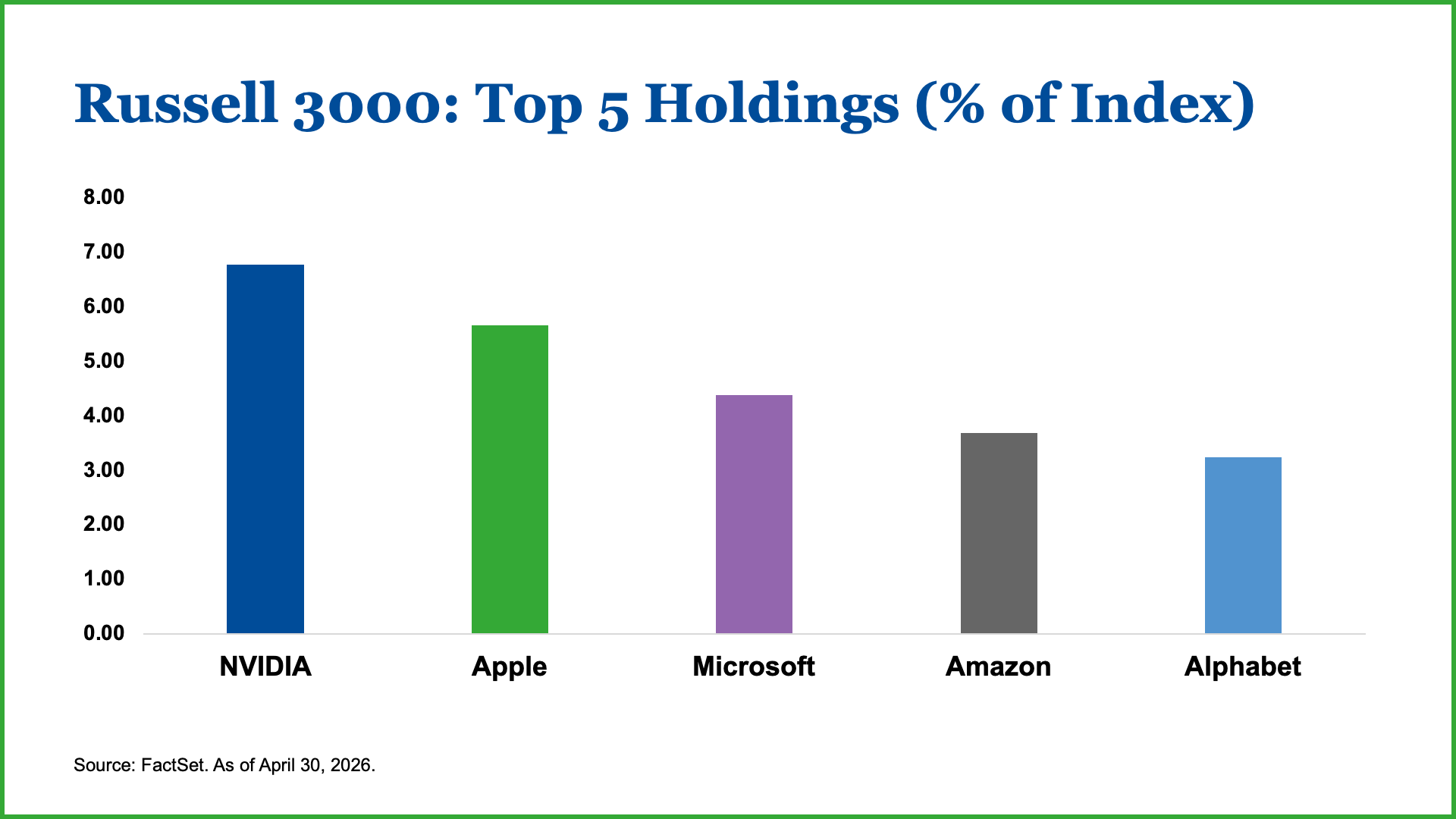

Figure 1

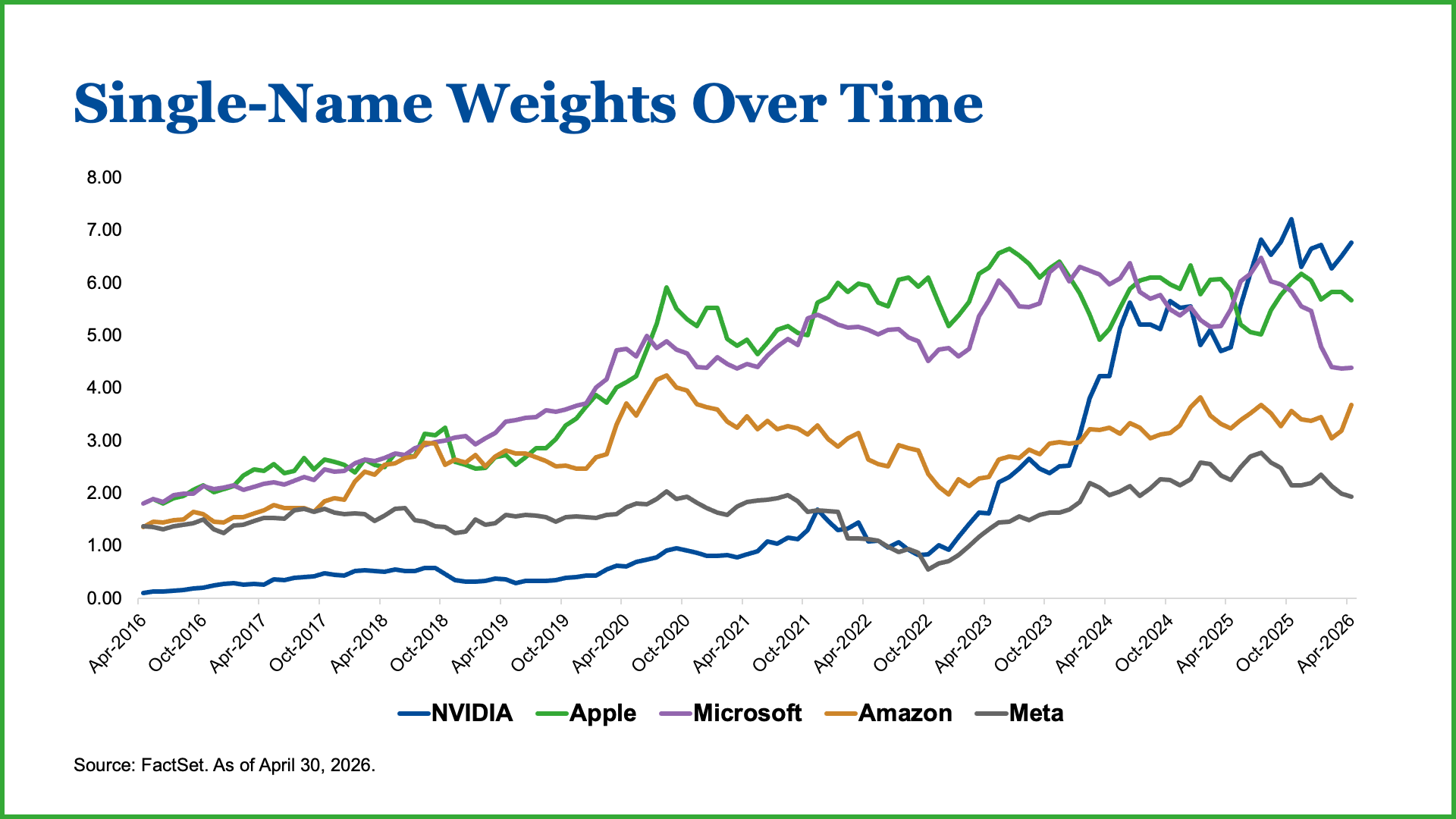

In Figure 1, the top five names in the Russell 3000, our preferred measure of the broad U.S. equity landscape, represent almost 25% of the index, as of April 30, 2026. These companies’ weights over time have clearly increased over the past 10 years, as shown in Figure 2.

Figure 2

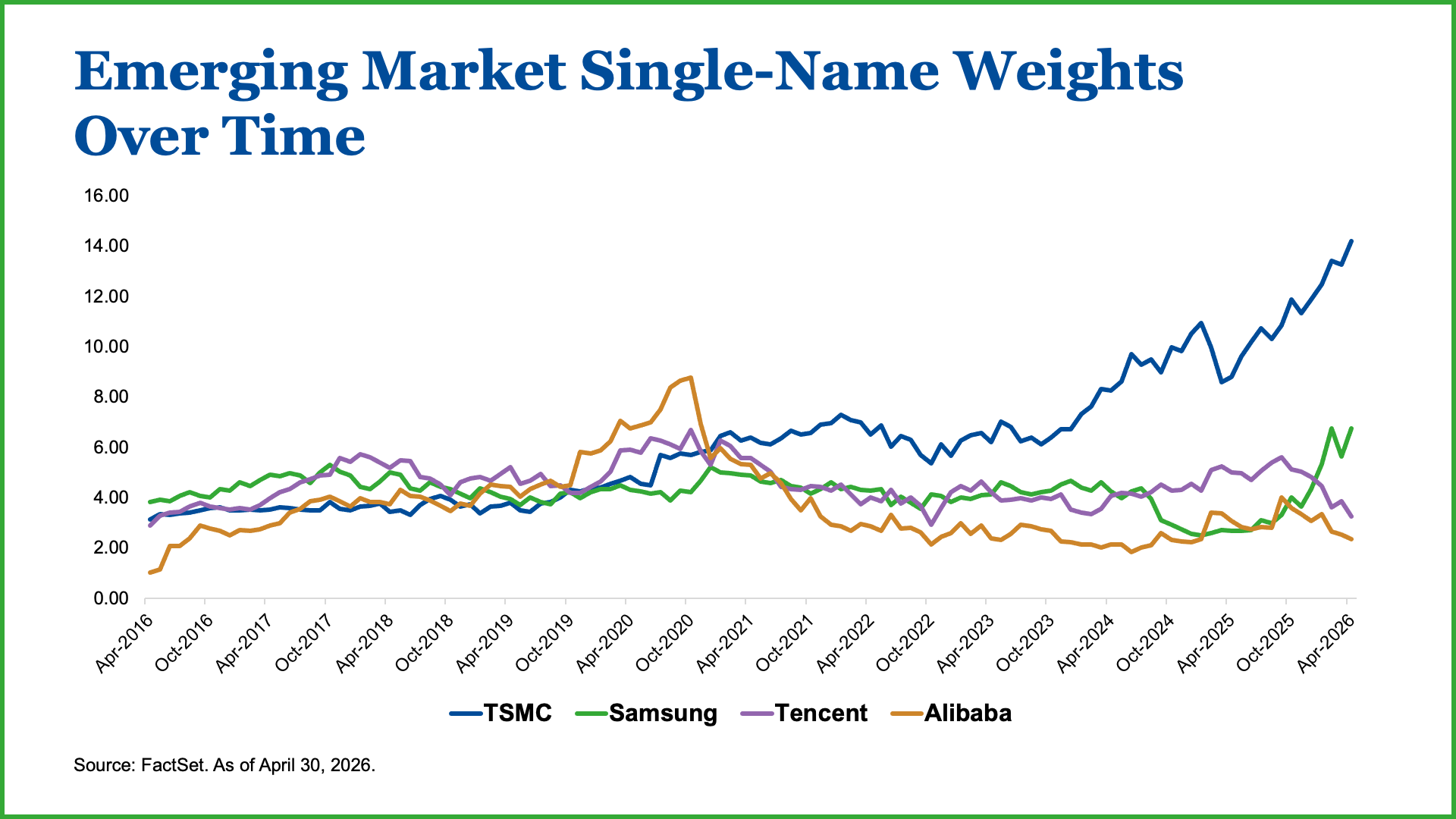

When we look at emerging markets, we see an even more concentrated view as demonstrated in Figure 3.

Figure 3

TSMC is now almost 15% of the emerging market index (and 41% of the Taiwanese stock exchange). To put that in context: TSMC attracts about one dollar for every seven invested in an emerging market index.

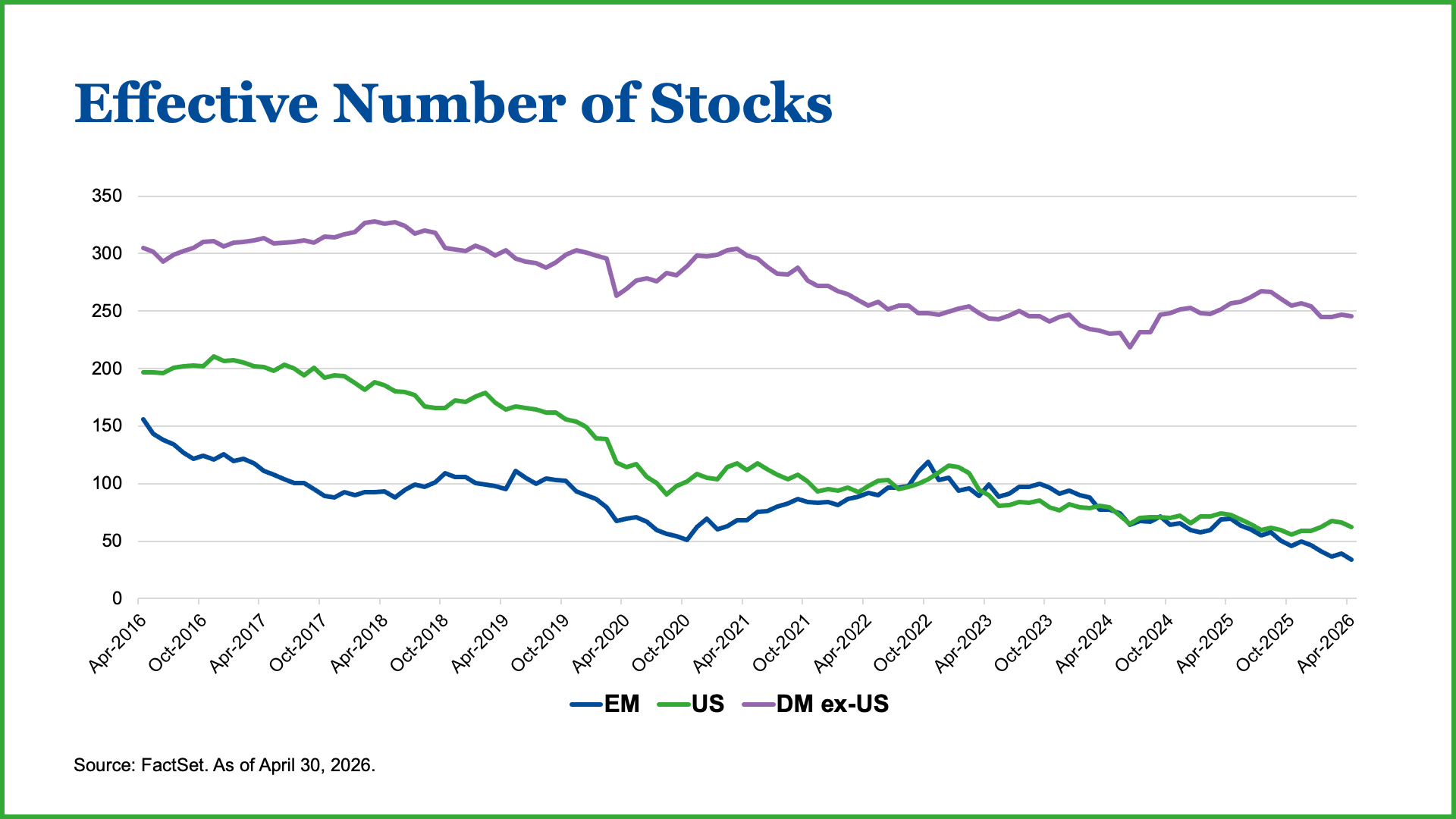

Economists use a measure called the inverse Herfindahl index to measure the effective number of companies tracked by a market index. The inverse Herfindahl index tells you how many equal-sized competitors it would take to match the current setup of a market or portfolio, translating concentration measurements from a percentage into a simple, real-world headcount. In the case of the emerging market index, the inverse Herfindahl index shows there are just approximately 34 companies tracked, as shown in Figure 4.

Figure 4

In other words, an index that is expected to track 24 emerging market countries, with over 1,200 constituents, is effectively only covering 34 companies. Similarly in the U.S., we have seen the decline in effective number of stocks the Russell 3000 is tracking.

While this may look like a cause for concern, as noted previously, concentration historically comes in cycles. Thus, we don’t view heightened concentration as a concern outright. It’s emblematic of the market cycle that we’re in. It’s worth noting as allocators, and as an allocator with a disciplined, long-term perspective, that it’s important to glean any lessons and takeaways our experience might teach us. Here’s one: Amid high levels of concentration, there is surely a way to be more deliberate and effective when it comes to achieving diversification.

Concentration Risk Comes in Cycles

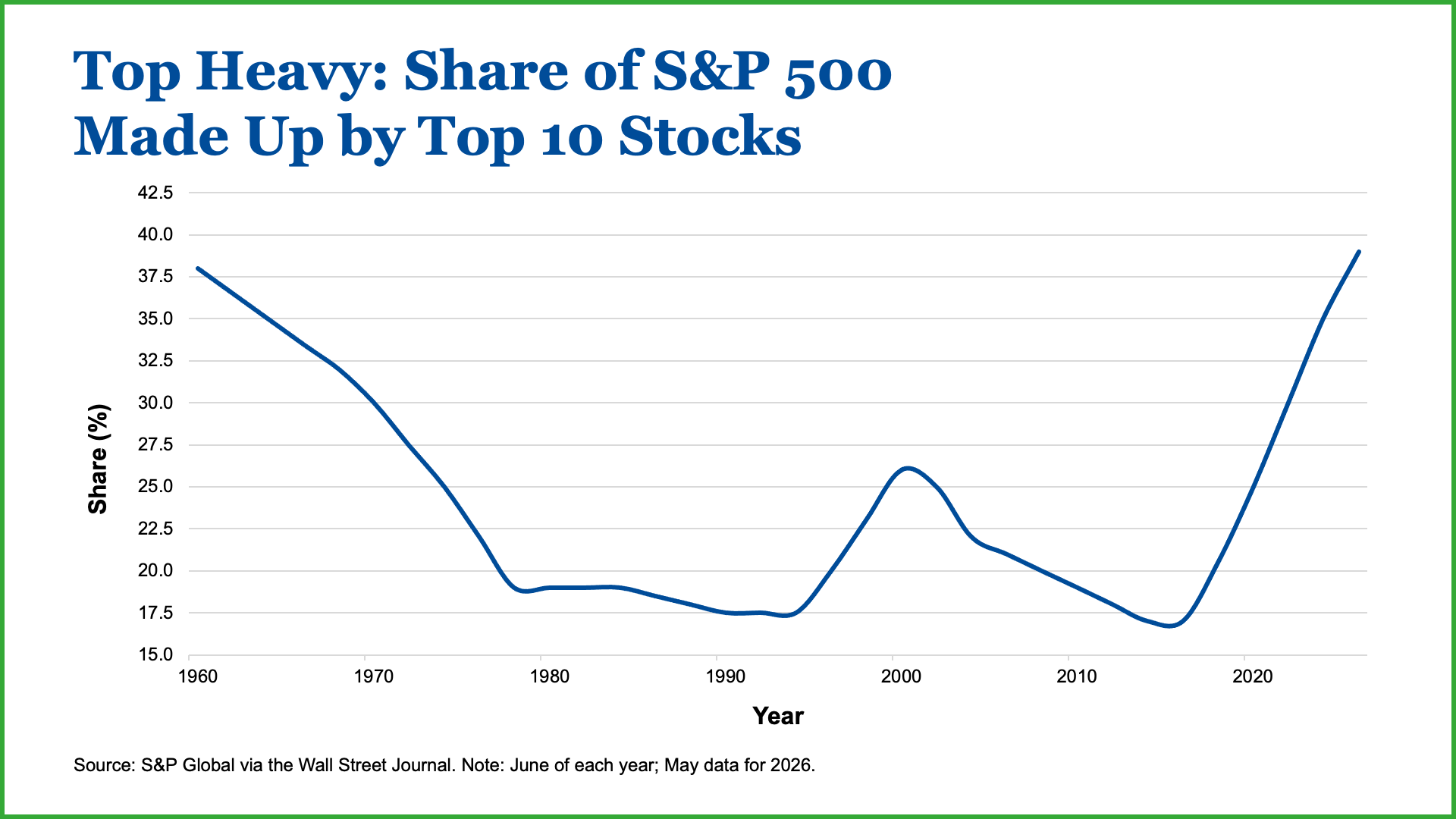

Today’s top-heavy market might feel extreme, but history indicates it’s a feature of market cycles. The Nifty Fifty of the late 1960s and early 1970s certainly had their technological advances (who can forget the credit card imprinter or what I am told used to be called the ZipZap machine?), but buying stocks easily and broadly was clearly more difficult back then. Yet, in that period, the top 10 companies comprised almost 40% of the S&P 500 (see Figure 5).

Figure 5

Of course, that this has happened before does not mean it is without risk. In the Nifty Fifty era, as in the dot-com boom decades later, both concentration and valuations were concerns… and they arguably are again today.

“Today’s top-heavy market might feel extreme, but history indicates it’s a feature of market cycles”

Concentration vs. Diversification

One popular argument in debates about index concentration is that, if one dominant theme or industry is taking up too much weight, the index course naturally corrects to attract capital to the next big thing. The issue is that course correction can be quite painful and can take quite some time.

Many investors look to diversification to ease the pain here. Spreading across different themes, geographies and sectors is, of course, important. But during these periods, cross-asset correlation, wherein companies in different industries or regions are moving in similar directions more than they used to, can become a bigger factor.

As each additional holding buys less genuine independence, the risk of over-diversification increases, where adding an additional company counter-intuitively adds risk in the portfolio. Managing this pendulum is a balanced blend of art and science. Every portfolio decision is an active one – even the decision to invest passively. For example, choosing an index fund is still a choice.

Where the concentration risk is hiding

Concentration risk isn’t just about what’s in the index – it’s about who builds the index. One area that concentration won’t show up in a chart is the index providers themselves. MSCI, FTSE Russell, Nasdaq and the S&P are the decision makers upstream that determine what goes into those funds that affect millions of investors.

These providers determine guidelines, set classification rules, decide timelines and requirements for new listings to be included in their indices. And because trillions of dollars track their indices mechanically, any changes move real money and economies.

These not-so-subtle flow examples are from The Economist:

- South Korean government bonds saw roughly $60 billion of foreign inflows tied to FTSE Russell’s decision to add them to its World Government Bond Index.

- Robinhood shares jumped ~16% in September on news they would join the S&P 500, a price driven by anticipated index buying, not earnings.

- Goldman Sachs projects that if MSCI reclassifies Indonesian stocks toward “frontier” rather than “emerging,” it may trigger an estimated ~$7.8 billion outflow from the market – not because anything is changing about the companies, but because of where a line got drawn.

Source: https://www.economist.com/finance-and-economics/2026/05/12/index-rebalancing-is-now-the-biggest-event-in-markets. Issue date: May 12, 2026.

What This Means for Investors

We have three takeaways given the concentration risks we see in the market:

One, it’s important for investors to monitor concentration measures, and build equity portfolios that can capture today’s biggest themes needs to be balanced with prudent risk management. Remember, as we saw in Figure 4, the Russell 3000’s breadth is not as wide as one might expect.

Two, diversify deliberately rather than reflexively. More names in a portfolio are not necessarily more diversification. We aim to build equity portfolios that take risk into consideration by building a lineup of complementary holdings – that is, companies that behave independently of each other, as much as possible.

Three, and perhaps most overlooked, in a fully passive portfolio, you have to pay attention to the institutions that are setting the rules. You are beholden to a handful of providers that end up making crucial decisions on where capital goes.

Concentration isn’t inherently risky. It needs to be put into context, monitored, and be part of a more holistic risk management playbook. Given the dominance of technology in the financial markets, and the broader economy, investment frameworks are overdue for a rethink. Investors should audit their portfolios for unintended concentration, specifically, whether they’re making an implicit bet on a single driver of returns. Fixed income investors should look through asset class labels to the underlying exposures. Equity investors should focus on where companies generate revenue, not where they’re listed.

The broader implication is a clear case for optionality. Blending index exposures with differentiated building blocks, and layering in a scenario-based approach, create the flexibility needed to navigate persistent economic uncertainty. A sound investment governance framework makes the trade-offs explicit: managing concentration risk, stress-testing singular-theme dependence, and ensuring the total portfolio is driven by underlying robust and long-term return drivers — not labels.

Data Sources: S&P Global via the WSJ as of 5/12/2026, FactSet as of 4/30/2026 and the Economist as of 5/12/2026.

This is not an offer to purchase securities or an investment recommendation. Please see the Investment Funds Description – I Series and Investment Funds Description – P Series for information about the Wespath funds.